GRAY ZONE

Traders see 1-in-6 odds of a NATO-Russia clash this year. But the real risk may lie in events that won’t trigger a YES resolution

Polymarket traders seem to be pricing a startling scenario: that the Russia-Ukraine war—Europe’s deadliest since World War II—could spiral into an even wider conflagration before year’s end.

Traders currently put the prospects for a “military clash” between NATO and Russian forces at about 17 percent. A die roll.

But what are traders actually pricing? And which events could be the most geopolitically consequential? I scanned the historical record and found some telling insights.

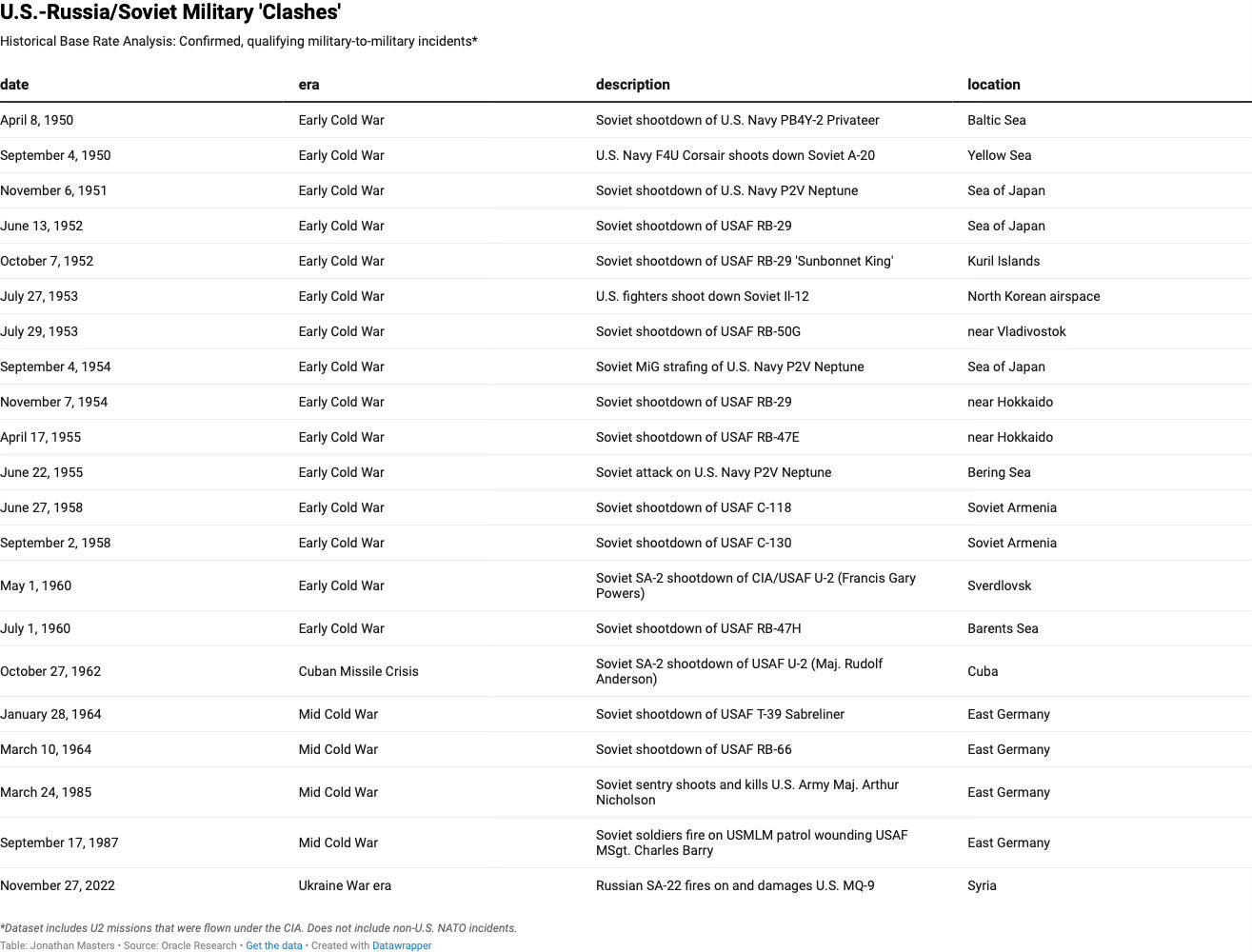

Base Rate

In a rough screening of the record since 1950, I found some 21 likely qualifying incidents involving the U.S. and Russia/Soviet Union, for a base rate of roughly 17 percent–very close to where the market today is pricing for a wider NATO-Russia clash.

But the bulk of these incidents occurred during the early years of the Cold War before satellites reduced the demand for risky overflight recon missions. Strip those out and the post-1965 rate drops to single digits, roughly consistent with the adjacent U.S.-Russia market today.

The fact that the broader NATO-Russia market prices nearly three times higher likely reflects the alliance’s vast membership, its proximity to a major land war, as well as incidents like Turkey’s 2015 shoot down of a Russian jet near the Syrian border.

More recent U.S.-Russia encounters involving Reaper drones (2022 over Syria; 2023 over the Black Sea) may hold the biggest clues to how these markets might trigger in the months ahead. If the targeting of larger, unmanned surveillance drones lowers the threshold for a qualifying incident while lowering the stakes of one, the satellite-era base rate may be too optimistic, and the “early Cold War” pricing may not be as crazy as it looks.

Close Calls

Both markets define a “military encounter” narrowly: a fairly unambiguous use of force/weapons by the Russian or U.S/NATO militaries against the other.

This has not happened near the Ukraine war since it began. But the rules exclude several provocative incidents that have, highlighting how much escalation risk sits outside the market. For example:

Intercepts of munitions targeting a third party*–During a massive Russian barrage against Ukraine last September, more than a dozen Russian Gerbera-type drones crossed into eastern Poland where several were destroyed by Dutch and Polish fighters. The episode was reportedly the first time that NATO aircraft destroyed hostile targets inside the alliance, and it prompted NATO Article 4 consultations (only the eighth in history).

Dangerous interference short of weapons use–A Russian fighter jet collided with a U.S. MQ-9 Reaper drone over the Black Sea in 2023, damaging its propeller and forcing it down. The incident brought Russian and U.S. military assets into direct physical contact for the first time during the Ukraine war.

Non mil-to-mil spillover–A Russian drone struck an apartment building in Romania in May, injuring two civilians. Again, an extraordinarily provocative event but clearly outside the markets’s rules.

Gray-zone attacks–All of the above is just one band of conventional military escalation risk in a much wider spectrum that includes unconventional Russian military, paramilitary, and intelligence operations (e.g. cyberattacks, sabotage, assassinations). Western analysts have documented a steep uptick in these types of Russian operations–often called gray-zone activities since the 2022 invasion.

Big Risks Below the Threshold

The record is somewhat reassuring about the risk for a catastrophic escalation: when qualifying mil-to-mil incidents do happen, they tend to be managed diplomatically.

But the increase in Russia’s gray-zone operations against NATO hints at a more insidious problem. One of Russian President Vladimir Putin’s strategic goals is to drive a wedge into NATO–particularly between the United States and European members–in order to undermine confidence in the alliance’s collective security guarantees.

Why would Moscow want an open military clash with NATO when it can keep probing the alliance through gray-zone activities, which are relatively low-cost, low-risk, and potentially more strategically valuable?

The danger is that more frequent and transgressive gray-zone actions by Russia repeatedly test and strain NATO’s collective response. A particularly egregious Russian operation, which some defense experts say could culminate in a limited ground incursion, might compel a NATO member to seek an Article 5 declaration.

What to Watch

There are a few things traders might want to track that would shift the risk environment around these markets and move the odds of a mil-to-mil encounter:

Rules of Engagement. NATO members have discussed altering the alliance’s classified rules for when and how allied forces engage Russian drones or aircraft, potentially allowing for a more forceful response. European states also have their own ROEs, and some, such as Lithuania, have already altered them. Any shift could matter for prediction markets.

Force posture. Watch whether NATO reinforces or reorganizes–as with Eastern Sentry– its eastern flank. More military assets on the alliance’s frontier could improve deterrence but also put more allied systems into the airspace most likely to see a qualifying incident. Meanwhile, the Trump administration’s recent cancellation of some planned military deployments to Europe underscores how quickly the American posture can shift.

Drone War. The scale and pace of the drone war in Ukraine, already extraordinary, continues to expand. The more drones both sides put into the air, especially near NATO borders, the greater the chance of military-to-military spillover. A qualifying clash in these markets may be most likely to begin with a UAV incident at the edge of alliance airspace.

* only applicable to the NATO-Russia market

Disclaimer

Nothing in The Oracle is financial, investment, legal or any other type of professional advice. Anything provided in any newsletter is for informational purposes only and is not meant to be an endorsement of any type of activity or any particular market or product. Terms of Service on polymarket.com prohibit US persons and persons from certain other jurisdictions from using Polymarket to trade, although data and information is viewable globally.

I think the real bet is here:

https://substack.com/@intellectualdorkweb/p-203497759

Confucius say: Everyone watches for the black swan. The smarter trade is often watching the flock of gray swans accumulating