The Hormuz Reopening Gap

The Brent-WTI spread has not caught up to Polymarket

This is a cross-post from Polymarket Institutional Research. To receive future issues, sign up here.

Polymarket’s Institutional Desk is scaling up. For information on block trades, market making, and commercial data sales on either our U.S. or international exchanges, contact Brooke Rizzetto at institutional@polymarket.com.

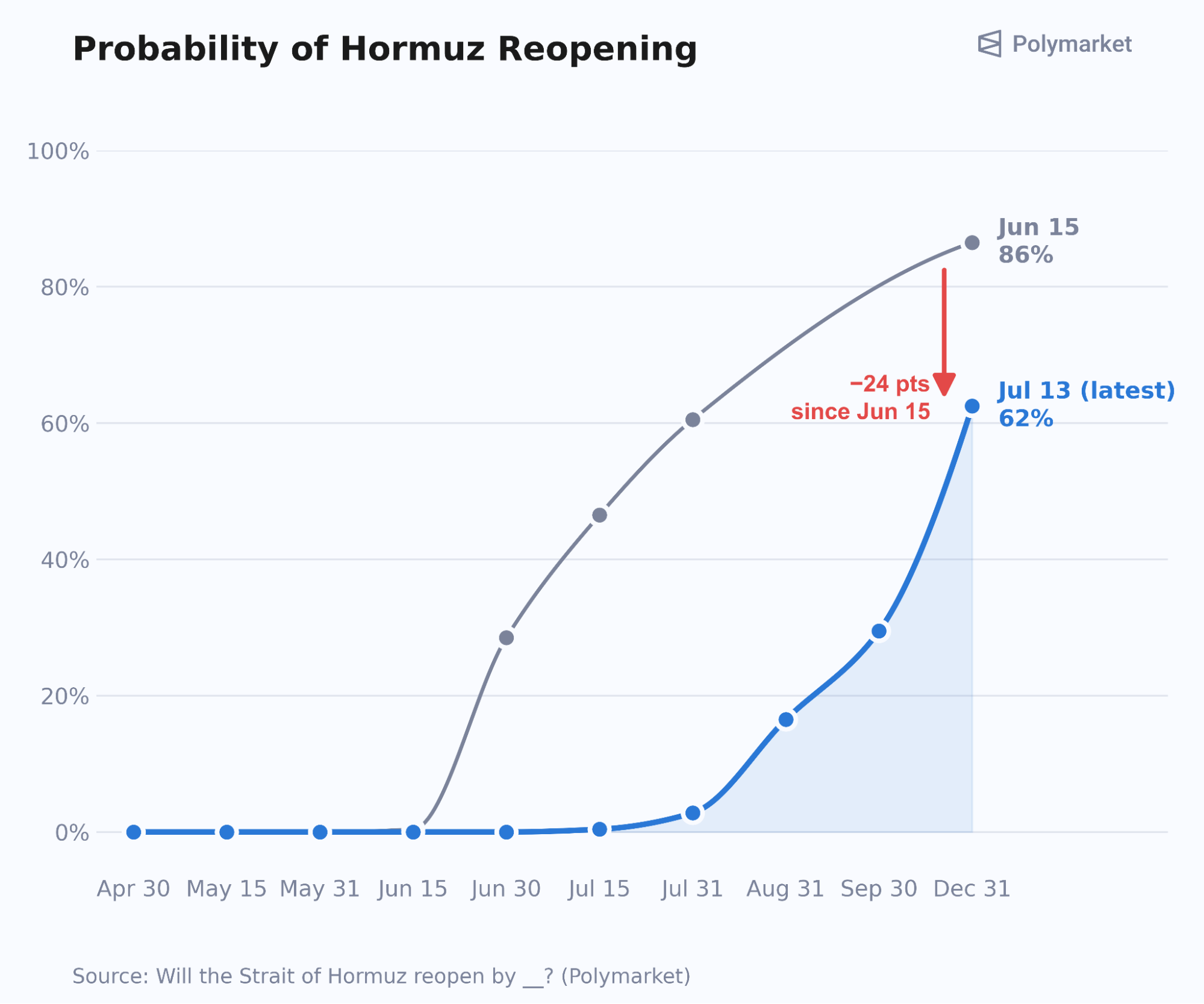

Pre-war, around 20 million barrels of oil flowed through the Strait of Hormuz daily. Polymarket traders now price a 62% chance for Hormuz normalization by year-end, defined as greater than 60 vessel transits recorded by IMF Portwatch on a 7-day moving average basis.

The latest 7-day moving average was 32, just over half the normalization threshold.

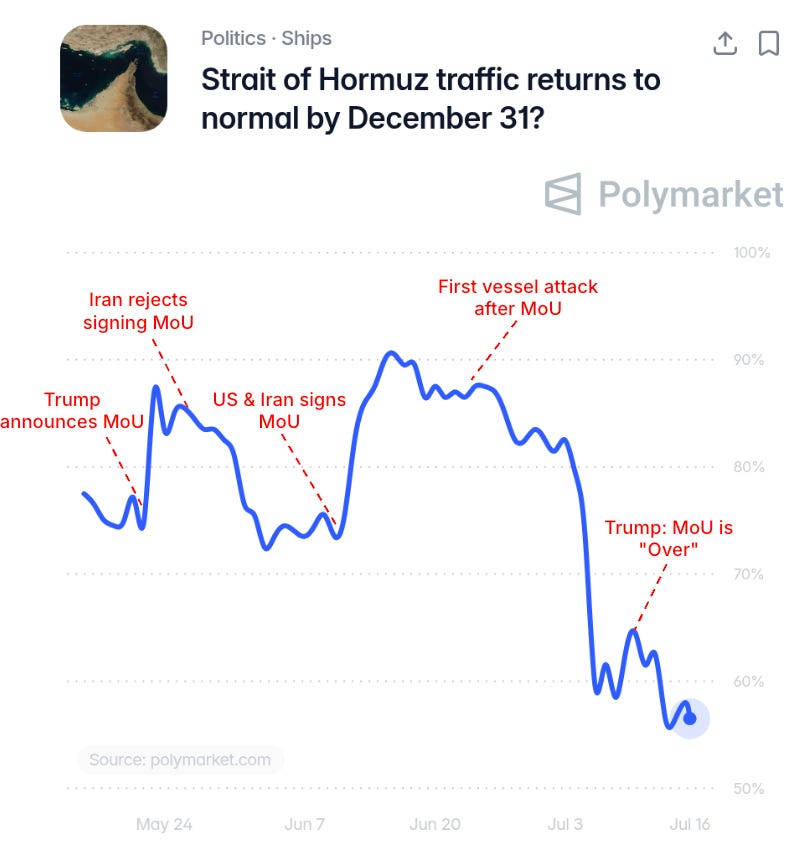

Over the past 30 days, year-end reopening odds have trended down, as traders grow skeptical of peace headlines and major differences remain over transit fees (Iran? U.S.?), and continued strikes on commercial vessels transiting the Omani lane.

What’s not priced in?

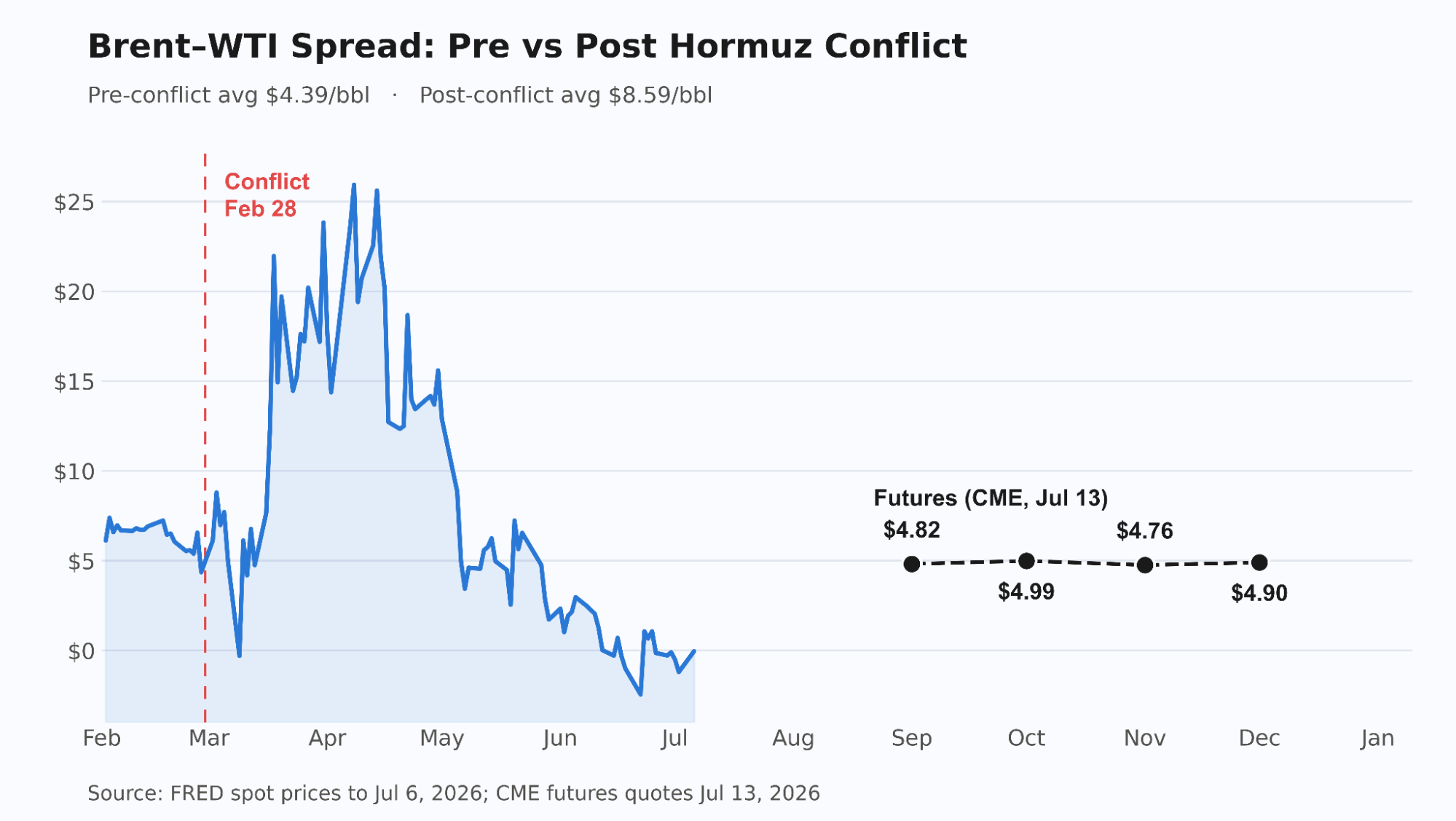

The chart above shows the realized Brent-WTI spread while the points from September to December are the forward futures curve. The break is where the historical data ends and market implied futures pricing begins. (Note: calculated daily from Brent-WTI settlement prices; conflict averages calculated since 28th February. December spreads are calculated from CME quotes.)

The spread between WTI and Brent oil benchmarks is widely seen as a barometer of Hormuz stress, as Brent is more heavily impacted by Gulf crude prices, while WTI is mainly U.S.-based and has little exposure to Hormuz transit risk.

The Brent-WTI spread shot up from ~$4.39 pre-conflict to over $25 during the war’s peak in April.

On Polymarket, the Hormuz reopening curve gives a live read on where the Brent-WTI spread should be. If the Strait reopens, the spread should revert to its ~$4.39 pre-conflict level. If the conflict drags on, it can stay near the ~$8.59 average since the war began.

Polymarket’s odds can be used to estimate the fair spread. At Polymarket’s 62% reopen and 38% prolonged closure, the fair spread is calculated to be ~$5.99.

Fair spread = [0.62 x $4.39 (pre-conflict spread)] + [0.38 x $8.59 (prolonged conflict)] = ~$5.99

Today, the December Brent-WTI spread trades at ~$4.90, well below the calculated fair spread. Should the year-end reopening odds continue to drop, the logical trade is to long the Brent-WTI spread near $4.90, using ~$5.99 as the fair-value anchor, with more upside should the reopening odds fall further.

Related Polymarkets

Disclaimer

Nothing in The Oracle is financial, investment, legal or any other type of professional advice. All odds are time-sensitive and subject to change. Anything provided in any newsletter is for informational purposes only and is not meant to be an endorsement of any type of activity or any particular market or product. Terms of Service on polymarket.com prohibit US persons and persons from certain other jurisdictions from using Polymarket to trade, although data and information is viewable globally.

| A guest post by

|

Great post! Does Poly have Brent/WTI spread market? Didn't see one on search.

Fascinating mismatch between Polymarket odds and Brent‑WTI futures. If reopening probability keeps falling, does the spread reprice quickly, or are energy traders discounting prediction markets altogether?