PILL MILL

The art & science of FDA drug forecasting

At this time last year, Polymarket traders thought FDA approval of a new kidney drug was almost a sure thing. YES shares traded as high as 89% before crashing to zero in days.

The strangest part? The drug was completely fine.

The drug in question, Unicycive’s oxylanthanum carbonate, was safe and effective. The problem was a third-party plant failing a manufacturing inspection. The FDA issued a Complete Response Letter (CRL), the agency’s “not yet” ruling that sends a drug back without approval, and the polymarket settled at zero.

This summer, that same molecule is back after resubmission, along with seven other FDA drug approvals.

The headlines may look similar, but these contracts are pricing completely different risks. One rides on whether a foreign factory passes re-inspection. Another rides on a Phase 3 readout, the big trial that decides whether a drug works as advertised. The trick is knowing which risk you’re holding.

Timing

Let’s start with the part that can be a bit misleading. Each of these polymarkets reads “FDA approves [drug] by [date],” and people trade it like a yes-or-no on the drug. But it’s actually all about the date.

Think of it like handing in a flawless essay a week past the deadline: you still get a zero, because the essay wasn’t the problem, the deadline was. A drug with a contract ending in June can clear the FDA months later in September, and its contract will still pay zero.

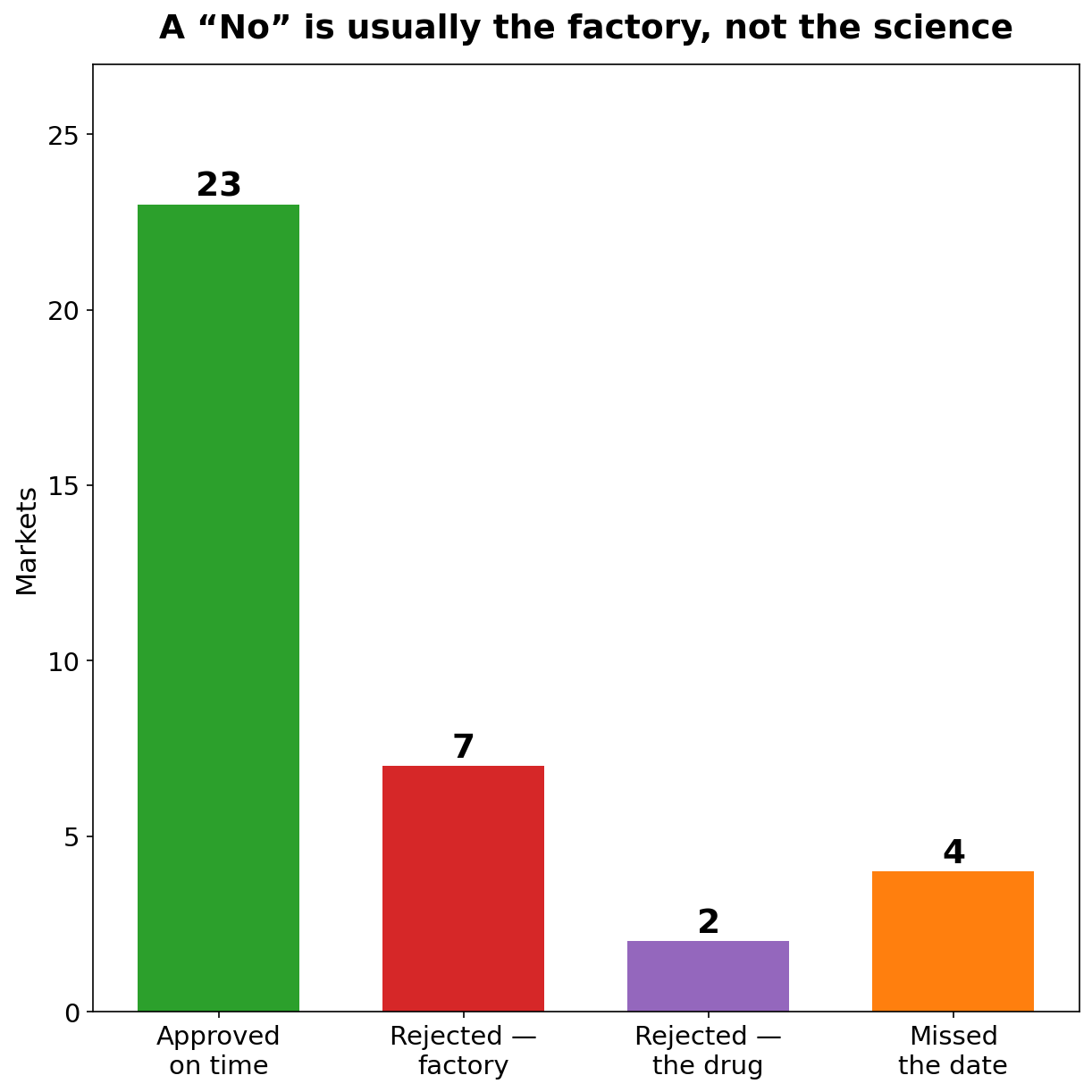

A NO on Polymarket isn’t always an FDA rejection. Of the 13 markets that resolved NO in our data, four were pure timing: a drug that simply required more time to work through the approval process.

Factory reset

And when a contract resolves NO on an actual rejection rather than a delay, the reason is usually dull. Of the nine CRLs in the resolved set, seven were manufacturing problems. Only two had anything to do with whether the drug worked.

A factory problem is also fixable. The company patches the deficiency, refiles, and takes another swing, which is why the same molecules come back for a second cycle.

Decoding FDA approvals

Before you even look at price, work through three things. First, the normal base rate: drugs that reach a decision get approved often, roughly 80% on the first cycle, and label expansions (where a drug is expanded to different diseases or demographics) are higher still.

Second, the designations: Priority Review (the FDA committing to decide in about six months instead of the usual ten) or a Breakthrough Therapy tag (an early flag for drugs showing unusually strong results) is the agency saying that it likes what it has seen. The base rate for these types of approvals is, again, higher than the usual.

Third, the prior cycle: if the drug received a CRL last time, find out why. A manufacturing fix is a far easier bar to clear than a fresh efficacy determination, and both lead to different expected approval rates.

Case Study: Oxylanthanum carbonate

Last June’s rejection came down to a single manufacturing deficiency at a third-party plant, with nothing said about the drug itself. Unicycive resubmitted in December to fix the issue.

So Oxylanthanum carbonate is back, and it’s a refile, meaning that they’re leaning on past data instead of re-running every trial to resubmit after their earlier CRL.

Thus, the Unicycive contract is really one question: does the refiled factory pass inspection before its July deadline?

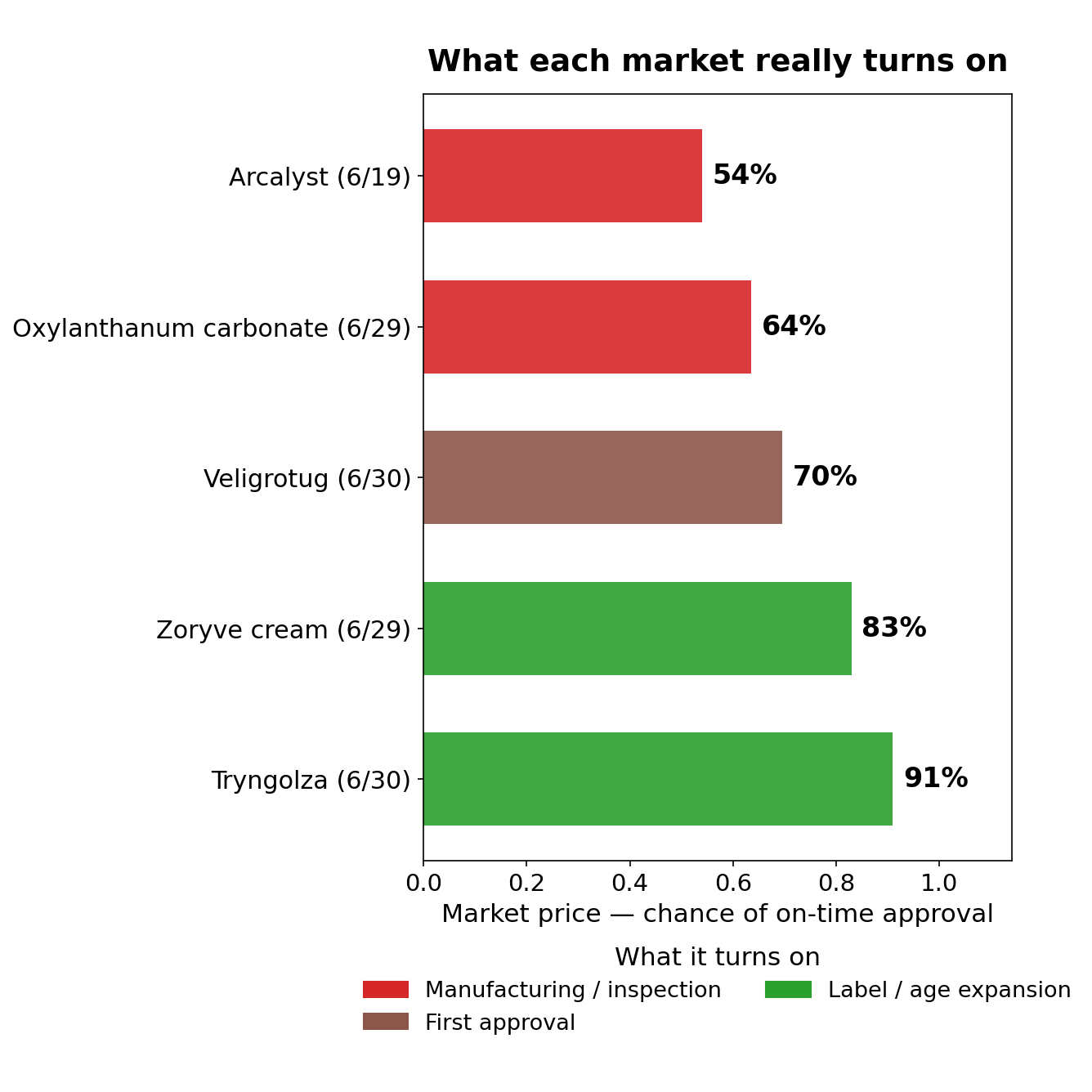

At 64%, traders are pricing that risk solidly below the approval base rate for a normal drug. (Note: at time of publication this contract’s orderbook showed a very wide spread, indicating a lack of trader consensus on the odds.)

The rest of the board

Armed with this knowledge of the base rates, let’s look at the other contracts that are live.

Two are clean reviews or expansions, and traders are pricing them like it. Zoryve cream at 83% and Olezarsen at 91% are first-cycle expansions with no manufacturing history to worry about. About as close to a formality as this category gets.

The key risk with Arcalyst (54%) hinges on a routine switch of manufacturing to a new contract plant, Samsung Biologics, for rilonacept, a drug that has never received a CRL, yet the crowd treats it as the riskiest trade on the board.

Only one drug is a first time approval. Veligrotug, at 70%, has good Phase 3 numbers and both Breakthrough and Priority Review, but first approvals carry more unknowns than expansions. It’s marked modestly below the usual base rate of 80%, for this reason.

Reading resolved markets

A few recently resolved markets also contain clues.

Just a few days ago, we had Oclaiz at 82% and Welireg at 84%. Close enough to look like the same trade, but three days later they’d gone opposite directions.

Oclaiz went first. On June 10, the FDA sent it back with a second manufacturing rejection tied to a third-party plant. Same story as oxylanthanum a year earlier. The contract priced at 82% fell to zero overnight, and NO shares paid more than fivefold. Again, it was the factory, not the drug that was the issue.

Welireg did the opposite. On June 12, it got approved: Merck’s belzutifan was cleared to widen into earlier-stage kidney cancer. A drug the FDA already trusted, on a trial it had already seen. The price drifted up and settled at a dollar: a routine label expansion.

Finally, Tebipenem was the only drug that rode on the molecule itself. It received a CRL on the science, was fixed with a fresh Phase 3 and approved June 17, clearing the most challenging FDA bar.

What’s next?

FDA forecasting hinges on a number of key risks: timing, factory approvals, new molecule approvals, and new use approvals (expansions). Each of these has its own base rate, which tends to outweigh drug-specific risks.

But this article looked at just 36 markets, too small to establish reliable base rates at that level of detail. We’ll tackle that in a future piece, digging into the broader historical record to build out a base rate for each individual risk.

How we built this

We pulled every FDA drug-approval market on Polymarket, open and resolved, and hand-checked the regulatory record behind each: application type, any prior CRL and its cause, designations, and the contract’s true resolve-by date, which carries a roughly two-week grace past the expected decision. Then we logged the price each market charged before its decision, anchored to the day the FDA acted rather than the later settlement. With 36 resolved markets the sample is small and skews toward contested, refile-heavy decisions, so read every number as directional.

Dataset and code: github.com/realakshayk1/fda-markets

About the Author

Akshay Kumar is a software engineer at Polymarket and a computational drug-discovery researcher at Penn, where he models tumor growth and drug response. He studies in the Life Sciences and Management program at the University of Pennsylvania, combining Wharton, biology, and data science.

Disclaimer

Nothing in The Oracle is financial, investment, legal or any other type of professional advice. All odds are time-sensitive and subject to change. Anything provided in any newsletter is for informational purposes only and is not meant to be an endorsement of any type of activity or any particular market or product. Terms of Service on polymarket.com prohibit US persons and persons from certain other jurisdictions from using Polymarket to trade, although data and information is viewable globally.

F**k yeah...this is just a phase...like overlooking the progression of molecules. So touché

wow this is so opium!! seeyuhhh 💯🧛♂️